Clur Shopping Centre Indices, Infographics & Press Releases

Clur Shopping Centre Indices, Infographics & Press Releases

The Clur Shopping Centre Index™ is derived from the Clur Collective™, an asset management industry standard, tracking performance at more than 5.4 million sqm of prime retail space across South Africa and Namibia, for listed and unlisted property funds.

“Continuing growth across all retail centre formats is being driven by a strong and increasing desire for human medicine via physical social and community interaction. Aligned growth in trading densities and base rentals signals that landlords and retailers are on a level playing field, after many years of disparity. A continued stable rent to sales ratio indicates ongoing controlled market risk.”

Belinda Clur

Founder & Managing Director

Clur International (Pty) Ltd

First quarter 2025

Small retail centres lead growth stakes

as Belief Economy emerges

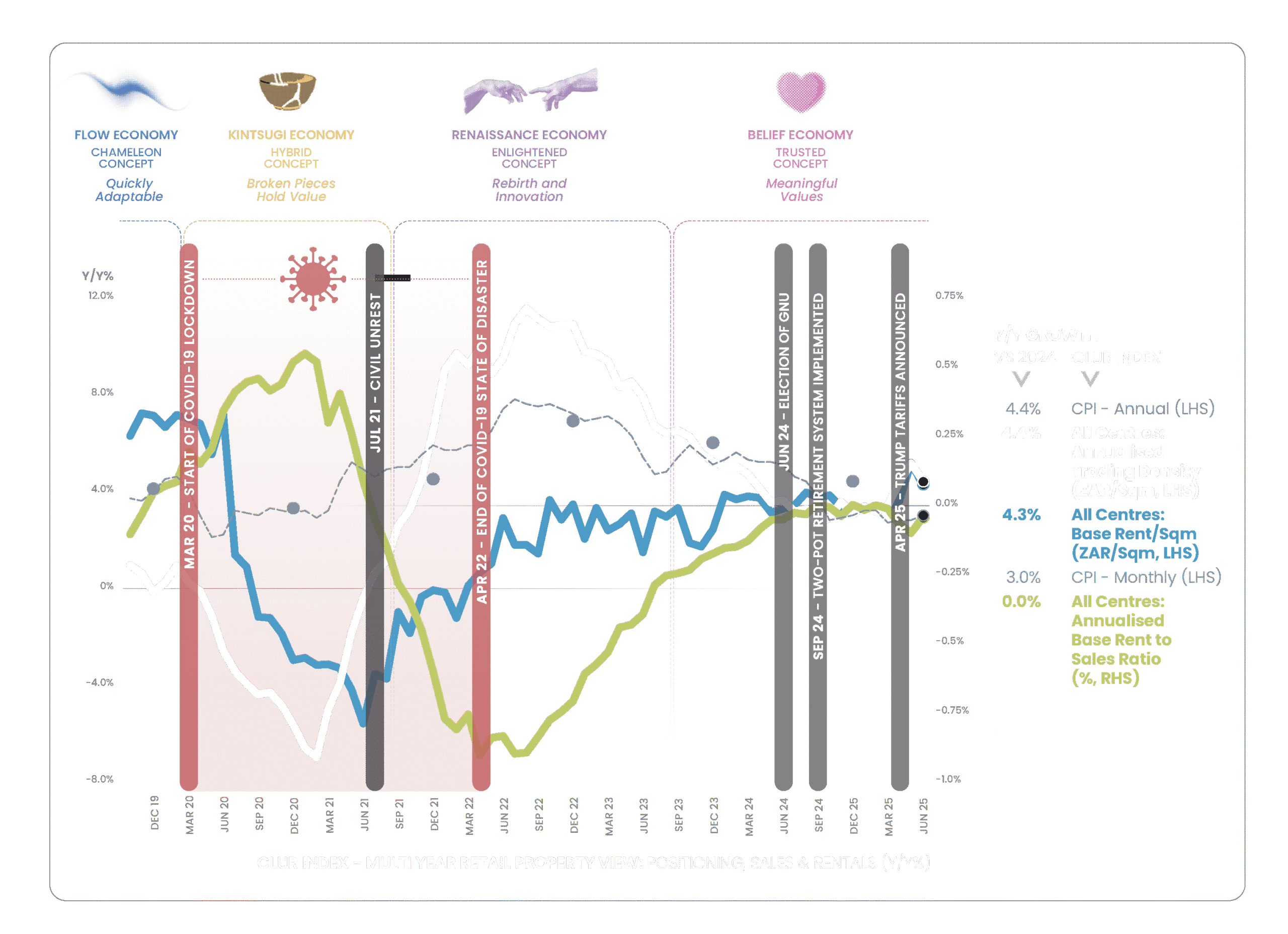

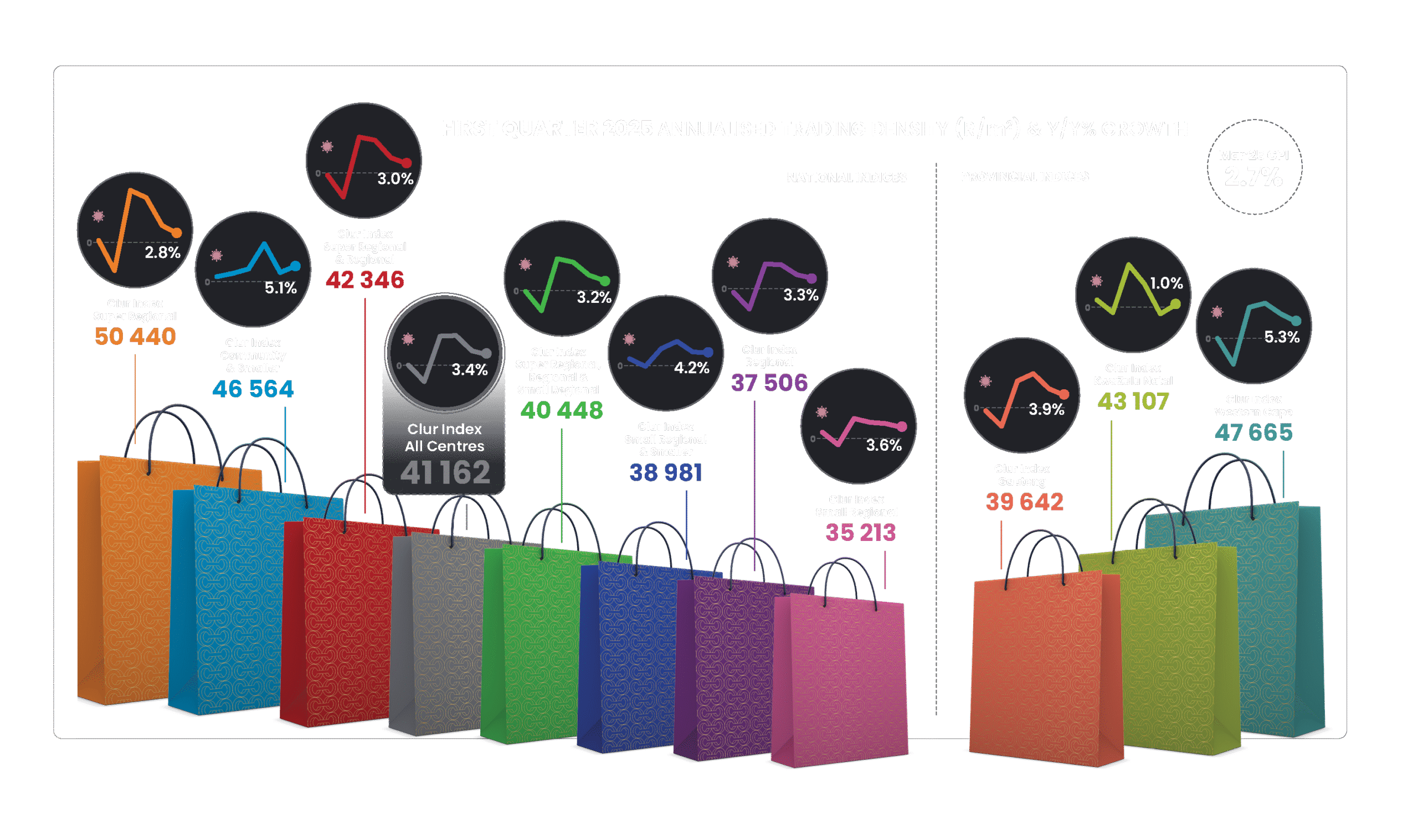

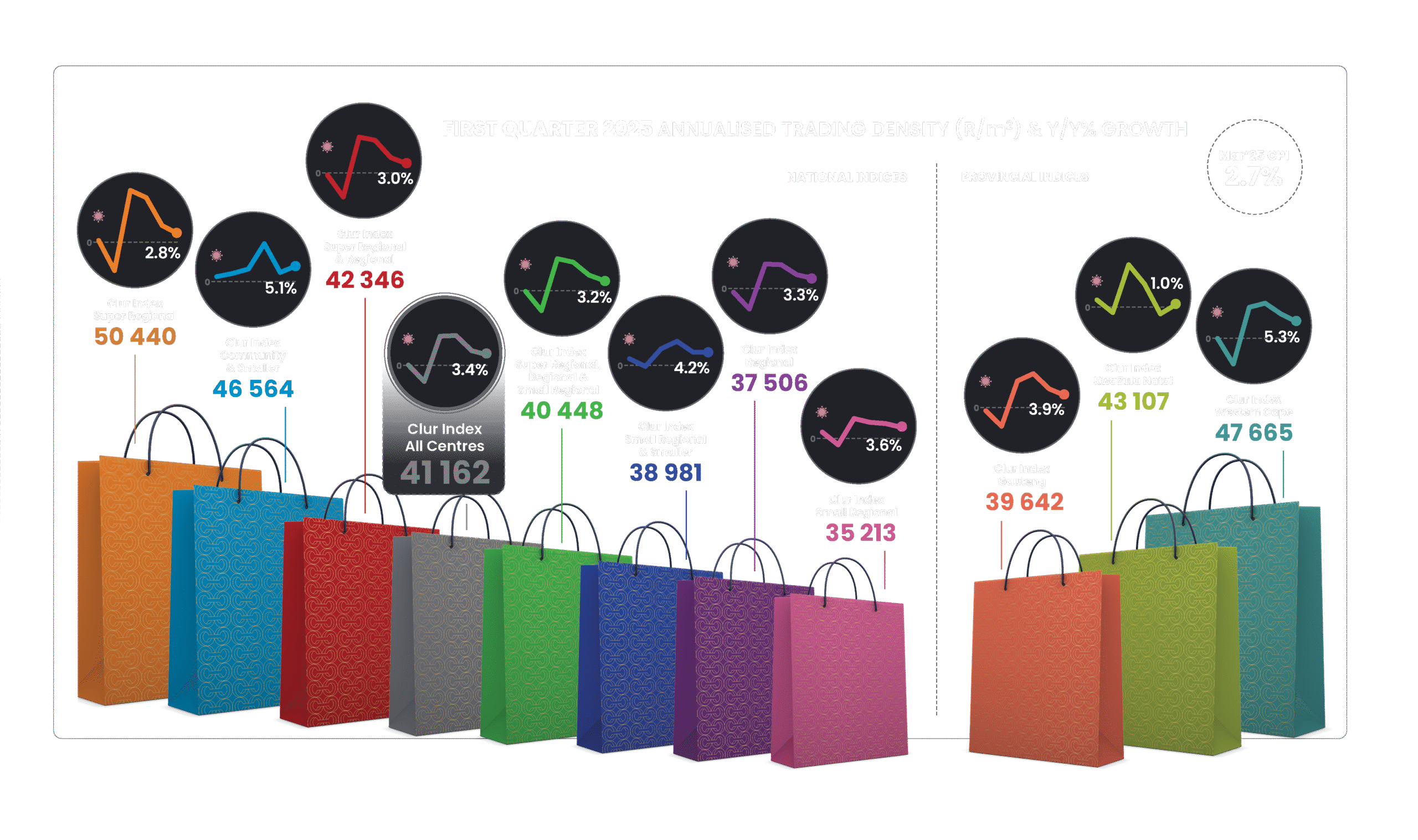

‘The Q1’25 national Clur Index outperformed Mar ’25 CPI and saw a growth expansion relative to Dec ’24, in terms of both annualised trading density and base rentals. The rent to sales ratio maintained its lowest level over five years, indicating ongoing stability and reduced market risk. Super Regionals, Community and Smaller Centres and the Western Cape stood out as top performing elements.

The consumer value system has shifted. A Belief Economy has emerged, the Attention Economy is fading out. Meaningful values are now prioritised over excessive exposure and trusted emotional and human connection is the new currency. This new Belief Economy is a critical positioning statement for future shopping centre and business strategies.’

Belinda Clur

Founder & Managing Director

Clur International (Pty) Ltd

Contact us

info@clurinternational.com

+27 (0) 78 038 1921

Clur International (Pty) Ltd

Clur Connect

Full year and festive season 2024

Industry closes 2024 and festive season

in good shape

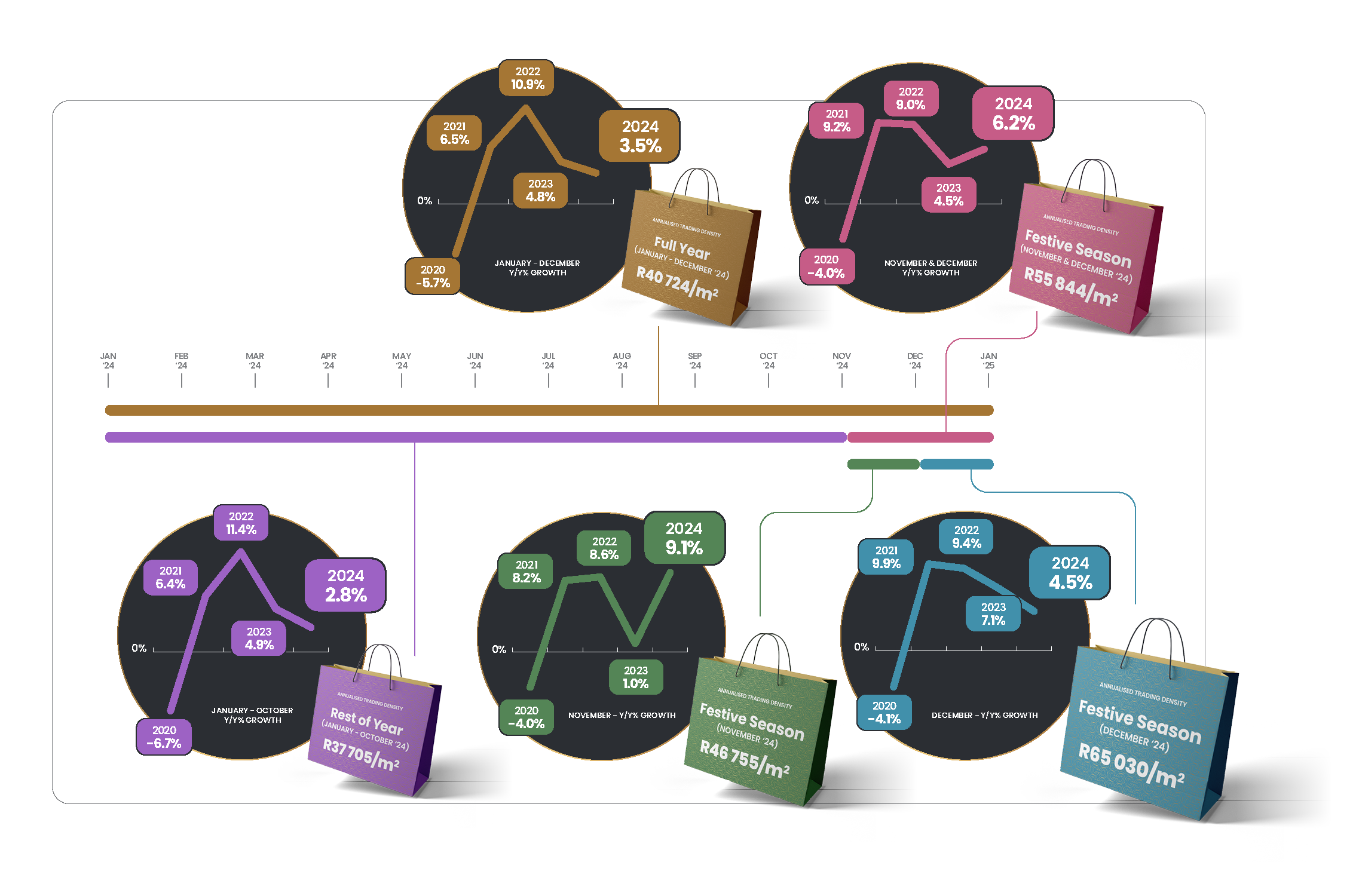

“2024 ended on a positive note, with growth in trading densities and rentals, and the further entrenchment of the lowest rent to sales ratio in 5 years, post Covid-induced volatility. Further, unwrapping festive season dynamics shows a stronger November than December trading growth position. 2024 also saw smaller centres shift to dominate the growth position of the industry.

The industry’s state of health seems to mirror the current consumer attitude towards wellness, which is one of the most important and defining trends to be considered in contemporary shopping centre strategy.”

Belinda Clur

Founder & Managing Director

Clur International (Pty) Ltd

Contact us

info@clurinternational.com

+27 (0) 78 038 1921

Clur International (Pty) Ltd

Clur Connect

The Clur Shopping Centre Index™ is derived from the Clur Collective™, an asset management industry standard, tracking performance at more than 5.4 million sqm of prime retail space across South Africa and Namibia, for listed and unlisted property funds.

“Continuing growth across all retail centre formats is being driven by a strong and increasing desire for human medicine via physical social and community interaction. Aligned growth in trading densities and base rentals signals that landlords and retailers are on a level playing field, after many years of disparity. A continued stable rent to sales ratio indicates ongoing controlled market risk.”

Belinda Clur

Founder & Managing Director

Clur International (Pty) Ltd

First quarter 2025

Small retail centres lead growth stakes

as Belief Economy emerges

“The Q1’25 national Clur Index outperformed Mar ’25 CPI and saw a growth expansion relative to Dec ’24, in terms of both annualised trading density and base rentals. The rent to sales ratio maintained its lowest level over five years, indicating ongoing stability and reduced market risk. Super Regionals, Community and Smaller Centres and the Western Cape stood out as top performing elements.

The consumer value system has shifted. A Belief Economy has emerged, the Attention Economy is fading out. Meaningful values are now prioritised over excessive exposure and trusted emotional and human connection is the new currency. This new Belief Economy is a critical positioning statement for future shopping centre and business strategies.”

Belinda Clur

Founder & Managing Director

Clur International (Pty) Ltd

Full year and festive season 2024

Industry closes 2024 and festive season

in good shape

“2024 ended on a positive note, with growth in trading densities and rentals, and the further entrenchment of the lowest rent to sales ratio in 5 years, post Covid-induced volatility. Further, unwrapping festive season dynamics shows a stronger November than December trading growth position. 2024 also saw smaller centres shift to dominate the growth position of the industry.

The industry’s state of health seems to mirror the current consumer attitude towards wellness, which is one of the most important and defining trends to be considered in contemporary shopping centre strategy.”

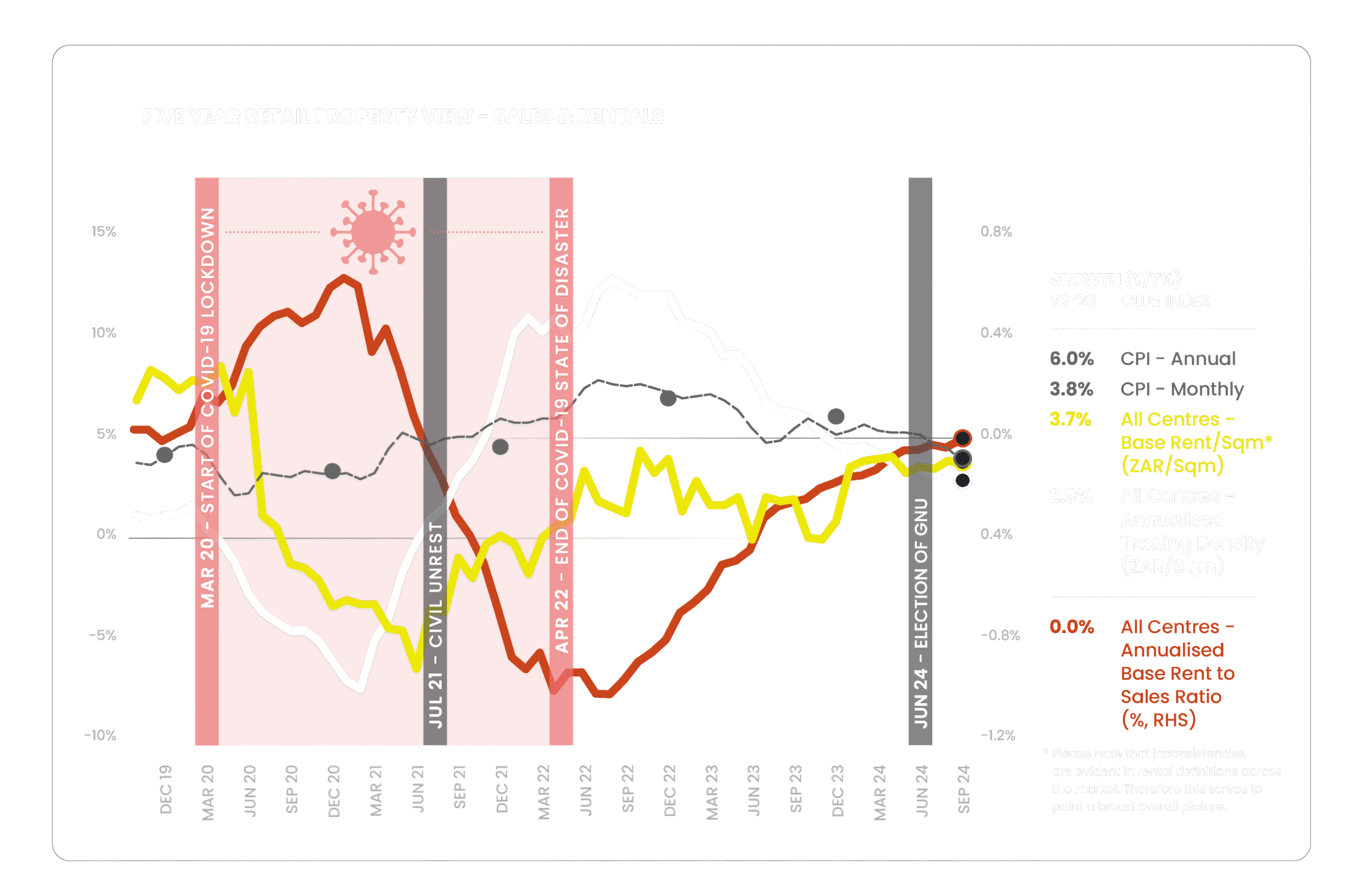

“The Clur Index for Q3’24 shows the gap between base rental growth rates and CPI is closing. Rental growth rates at Sept ’24 were at 3.7%, only 0.1% below relative CPI of 3.8%. Rental growth rates have consistently under-performed CPI since July 2020. They have also consistently under-performed annualised trading density growth rates from April ’21.

However, Q3 ’24 confirmed a change in this trend with rental growth outperforming annualised trading density growth throughout. Annualised trading density growth closed the quarter at 2.9%. The expected inverse relationship between trading density and the rent to sales ratio is also apparent. This overall position has been driven by a continued retreat in domestic inflation, a solidification in rental growth at above 3% over 2024 and a further contraction in annualised trading density growth in Q3 ‘24.”

Belinda Clur

Founder & Managing Director

Clur International (Pty) Ltd

Second quarter 2024

Community and Smaller Centres

shine as new retail frontier emerges

“Trading densities at Community and Smaller Shopping Centres were a bright spot in Q2 ‘24, running counter to a further contraction in retail property performance and supporting an important current theme of community and global wellness. With the emerging importance of the move to make the world well, community focused retail, as a new frontier, is a critical consideration for shopping centre strategy. This community spirit is signalling the need for social impact retail.

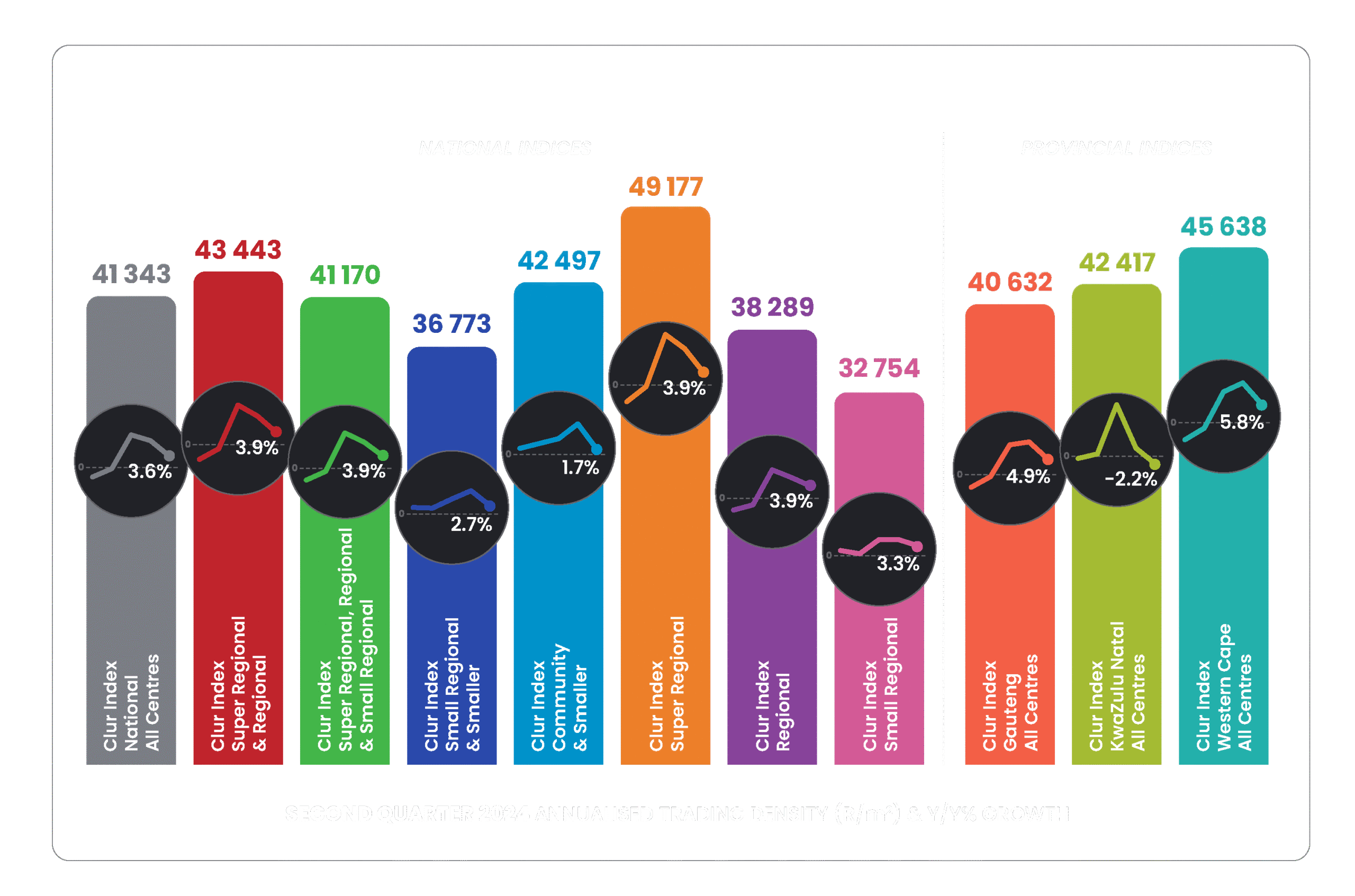

The Q2 ‘24 national Clur Index for All Centres closed at an annualised trading density of R41,343 /sqm, and y/y% growth of 3.6%. This represents a further contraction of -0.9% relative to Q1 ‘24 and -1.5% relative to the 2023 calendar year. This growth under-performed June ‘24’s CPI by -1.5%.

Highest trading densities were shown by the two size extremes of Super-Regional Centres and Community and Smaller Centres. Highest y/y% growth was shown by Super-Regional and Regional Centres. Community and Smaller Centres showed the lowest growth rate of the pack, but were the only segment to show an expansion in growth versus the first quarter. The Western Cape was the top provincial performer, and the only index to outperform June ‘24’s CPI. KwaZulu Natal was the only province to show a growth expansion versus Q1. Gauteng had the lowest provincial trading density and second highest growth rate.”

Belinda Clur

Founder & Managing Director

Clur International (Pty) Ltd

First quarter 2024

Shopping centre trading shows

softer dip in Q1 2024

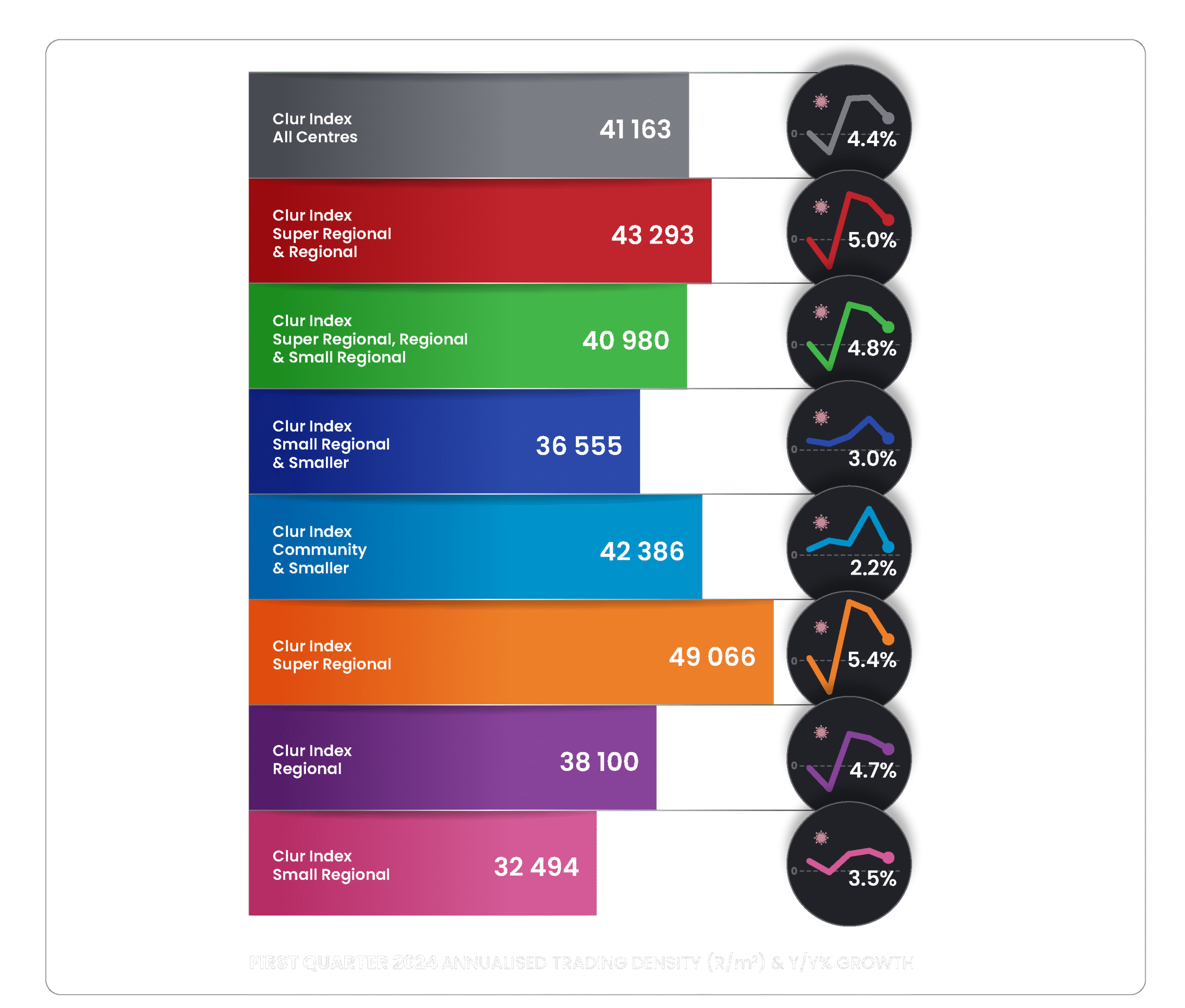

“The Q1 2024 national Clur Index for All Centres closed at R41 163/sqm and 4.4% y/y growth. This represents a contraction of 0.6% relative to 2023’s 5% y/y growth, but the rate of contraction was more muted than in H2 2023. The index has underperformed CPI since November 2023.

Super Regional centres (100 000 sqm plus) and Community & Smaller centres (below 25 000 sqm), showed the highest trading densities for the first quarter. This reflects top strength at the two size extremes of shopping centres, and may be linked to identity.

Larger Super Regional and Regional centres showed the highest growth rates. Regional centres were resilient, and Small Regional centres showed an expansion over the quarter.”

The Clur Index for Q3’24 shows the gap between base rental growth rates and CPI is closing. Rental growth rates at Sept ’24 were at 3.7%, only 0.1% below relative CPI of 3.8%. Rental growth rates have consistently under-performed CPI since July 2020. They have also consistently under-performed annualised trading density growth rates from April ’21. However, Q3 ’24 confirmed a change in this trend with rental growth outperforming annualised trading density growth throughout. Annualised trading density growth closed the quarter at 2.9%. The expected inverse relationship between trading density and the rent to sales ratio is also apparent. This overall position has been driven by a continued retreat in domestic inflation, a solidification in rental growth at above 3% over 2024 and a further contraction in annualised trading density growth in Q3 ‘24.